Investing wisely is one of the most crucial aspects of financial planning. Among the plethora of investment options available, Unit Linked Insurance Plans (ULIPs) and Systematic Investment Plans (SIPs) stand out due to their unique benefits and long-term wealth-building potential. Though both these investment routes address those searching for financial gains, they vary sharply in nature, objective, risk, and yields.

What is a ULIP?

A Unit Linked Insurance Plan or ULIP is an insurance policy that offers insurance coverage along with investment benefits. ulip allows the investor to place money inch amp run of finances such as arsenic debt fairness or stable finances and get spirit policy insurance

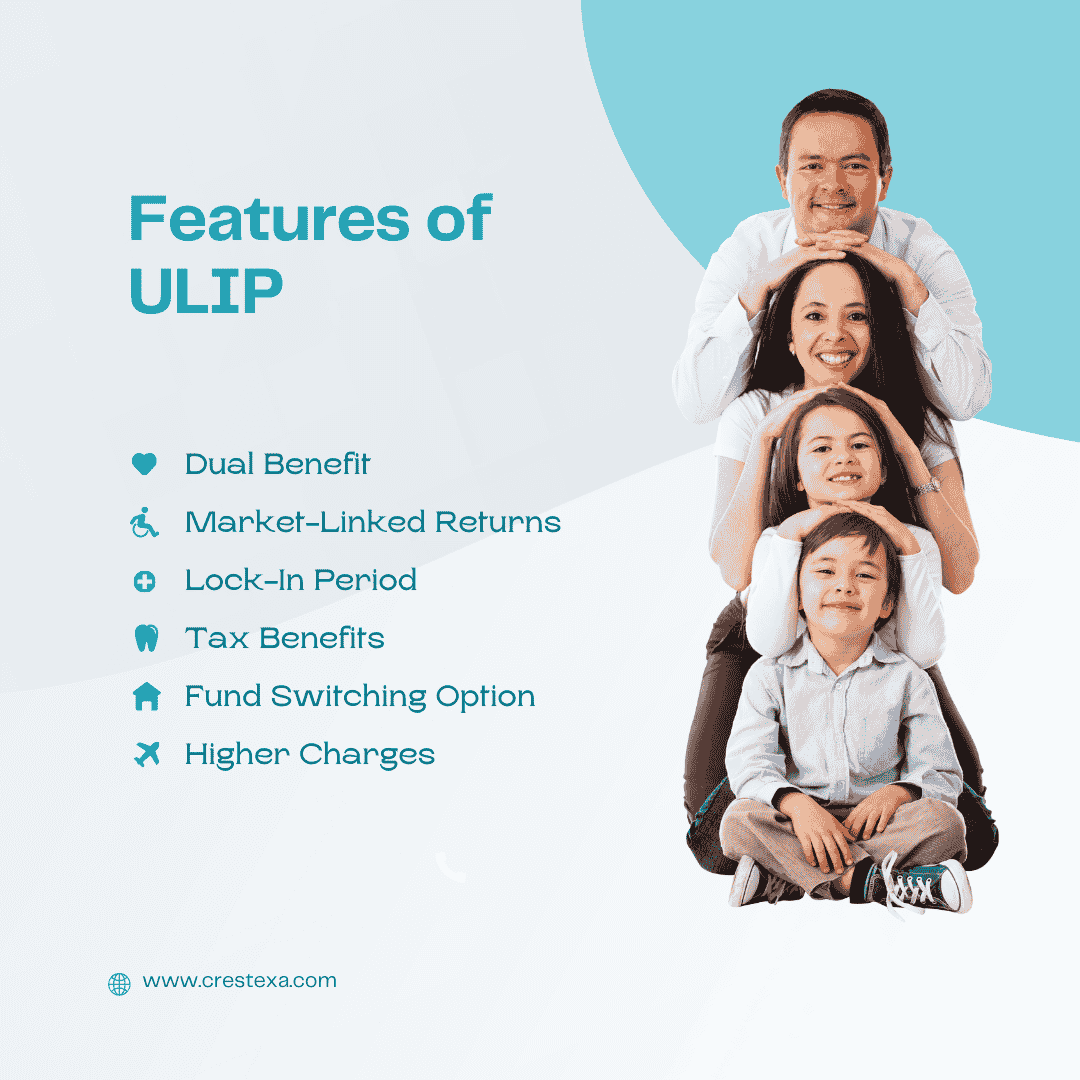

Features of ULIPs:

- Dual Benefit – ULIPs provide life insurance along with an investment option.

- Market-Linked Returns – Returns depend on market Effectiveness as funds are invested in equity debt or hybrid funds.

- Lock-In Period – ULIPs typically have a 5-year lock-in period, ensuring disciplined savings.

- Tax Benefits – Premiums paid for ULIPs qualify for tax deductions under Section 80C of the Income Tax Act, and maturity benefits may be tax-free under Section 10(10D).

- Fund Switching Option – Investors can switch between equity, debt, or balanced funds based on market conditions.

- Higher Charges – ULIPs have charges like mortality fees fund management charges and policy administration charges

Who Should Invest in ULIPs?

- People who are interested in long-term financial planning with cover against death

- Investors are ready to take a moderate-to-high level of risk for enhanced returns.

- People are interested in tax relief in addition to the creation of wealth.

Also Read : Bookkeeping Basics for Small Business Owners

What is a SIP?

A Systematic Investment Plan (SIP) is a disciplined investment strategy that allows individuals to invest a fixed sum in mutual funds at regular intervals, typically monthly or quarterly. SIPs offer a hassle-free way to participate in the stock market and build wealth over time.

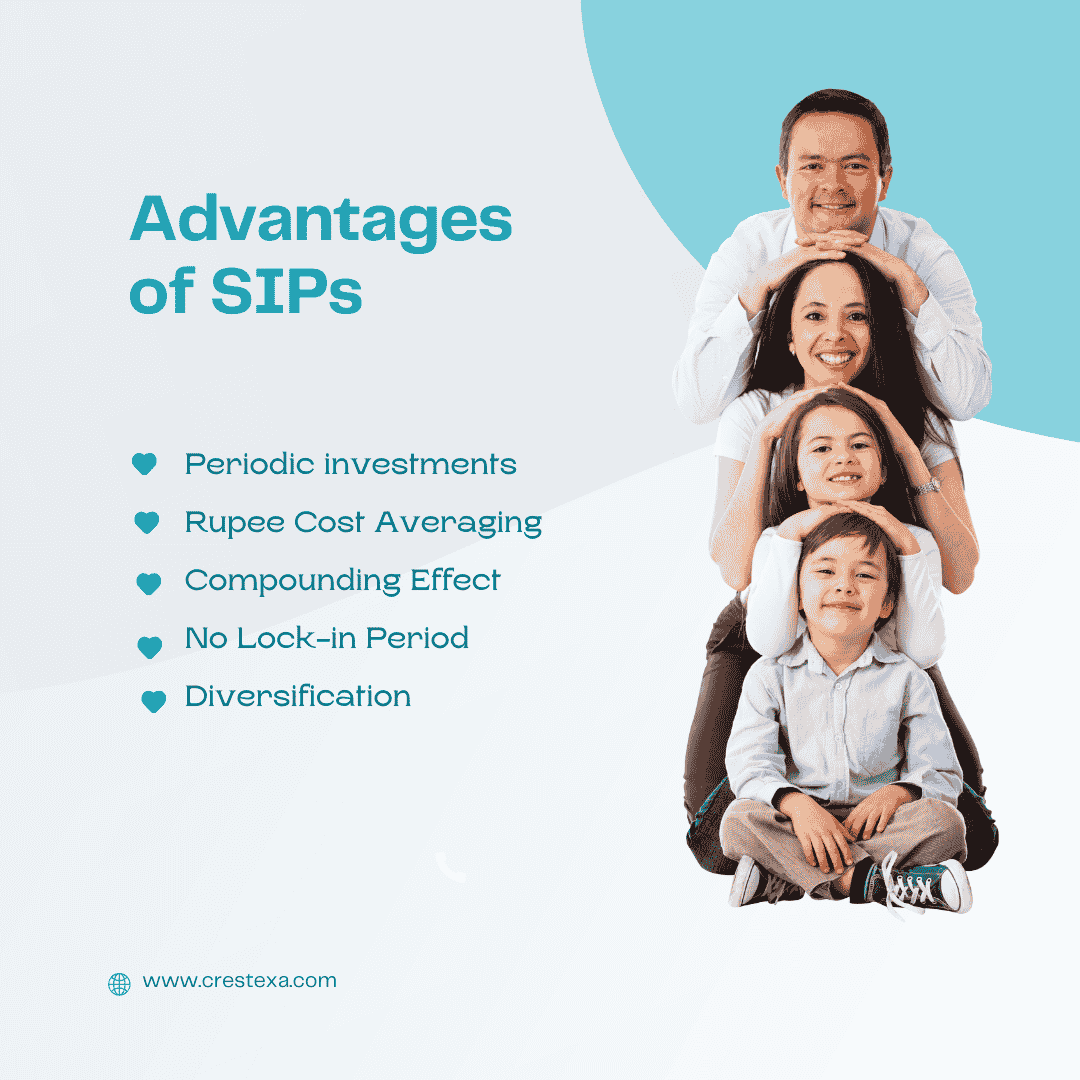

Advantages of SIPs:

- Periodic investments – Investors can initiate investment with as little as ₹500 every month, so everyone can invest.

- Rupee Cost Averaging – One purchases more units when prices are low and lesser when prices are high, limiting market volatility risk.

- Compounding Effect – Investments in SIP over the long run can create massive wealth because of compounding.

- No Lock-in Period – Contrary to ULIPs, most SIPs do not have a lock-in period, so liquidity is always available.

- Diversification – SIPs invest in mutual funds, which further invest in diverse asset classes, minimizing risk.

Who Should Invest in SIPs?

- Investors who want market-linked returns with flexibility.

- Investors who like liquidity in investments.

- Individuals who want a low-risk long-term investment strategy.

ULIPs vs. SIPs: Key Differences

| Feature | ULIP (Unit Linked Insurance Plan) | SIP (Systematic Investment Plan) |

|---|---|---|

| Purpose | Investment + Life Insurance | Pure Investment |

| Risk Level | Moderate to High | Low to High (depends on fund selection) |

| Returns | Market-linked | Market-linked (depends on fund) |

| Lock-in Period | 5 years minimum | No mandatory lock-in (except ELSS) |

| Tax Benefits | Under Section 80C & 10(10D) | Only ELSS funds offer tax benefits |

| Liquidity | Limited due to lock-in | High (funds can be withdrawn anytime) |

| Flexibility | Can switch between equity and debt | Choice of different mutual funds |

| Charges | Multiple charges (premium allocation, fund management, mortality) | Minimal charges |

| Suitability | Ideal for long-term planners with insurance needs | Best for wealth accumulation without insurance |

Charges Associated with ULIPs and SIPs

ULIP Charges:

- Premium Allocation Charge – Paid from the premium before investing.

- Fund Management Charge – As a percentage of the fund value, usually 1.35% annually.

- Mortality Charges – Premium paid for life insurance cover.

- Policy Administration Charge – Charged at regular intervals for policy servicing.

- Switching Charge – A few insurers charge charges for switching funds.

SIP Charges:

- Expense Ratio – Imposed by mutual funds on managing the funds.

- Exit Load – A small amount charged for early withdrawal (funds have varying exit loads).

- Fund Management Fees – Relatively lower compared to ULIPs.

Advantages and Disadvantages of ULIPs and SIPs

Advantages of ULIPs:

✔️ Twin advantage of life insurance + investment ✔️ Section 80C and 10(10D) tax advantage ✔️ Fund switching facility to realign in the event of changes in market trends ✔️ Long-term corpus creation ability

Drawbacks of ULIPs:

❌ Charge structure more expensive than SIPs ❌ Lock-in ensures liquidity is tied up ❌ Fund returns vary with the performance of funds

Advantages of SIPs

✔️ Easy and transparent investment process ✔️ High liquidity with no lock-in (with the exception of ELSS) ✔️ Less charges compared to ULIPs ✔️ Rupee cost averaging and power of compounding

Disadvantages of SIPs:

❌ No insurance protection ❌ Market-dependent returns resulting in volatility ❌ No tax benefits except investing in ELSS funds

Which One to Go For?

Choose between ULIPs and SIPs based on your investment horizon, risk appetite, and financial goals:

- If you are looking for insurance and investment in one product, ULIPs could be a better option.

- If you want flexibility, greater liquidity, and fewer expenses, SIPs are the best option.

- If tax savings matter, ULIPs offer greater tax advantages than SIPs.

- If you can accept market volatility, SIPs offer a simple method to accumulate wealth.

Difference in Taxation: ULIPs and SIPs

- ULIPs Taxation:

- Premiums paid qualify for deduction under Section 80C (up to ₹1.5 lakh per year).

- Maturity proceeds are tax-free under Section 10(10D) if the premium does not exceed 10% of the sum assured.

- Switching between funds within a ULIP is not taxed.

- SIPs Taxation:

- Equity Funds: 10% LTCG applies if gains are more than ₹1 lakh in a financial year.

- Debt Funds: Charged as per income tax slab for short-term gains; 20% with indexation advantage for long-term gains.

- Dividend Income: Charged as per investor’s income tax slab rate.

Which Is Suitable for Wealth Building in the Long Run?

- In case insurance protection is also required along with investment, ULIP is more preferable.

- If just higher returns and wealth creation is the sole agenda, SIP would be the optimal choice.

- For those who already possess adequate coverage of life insurance, SIP is a cheaper option.

- For investment and maximum tax gains, ULIPs may be contemplated.

Conclusion

Both ULIPs and SIPs have different financial uses, and the decision between them is based on your investment horizon, risk tolerance, and financial objectives. ULIPs are best for those who seek insurance coverage in addition to investments, whereas SIPs are best for those who seek higher returns with higher liquidity. Properly assessing the charges, taxation, and flexibility of both will assist in making an informed choice.